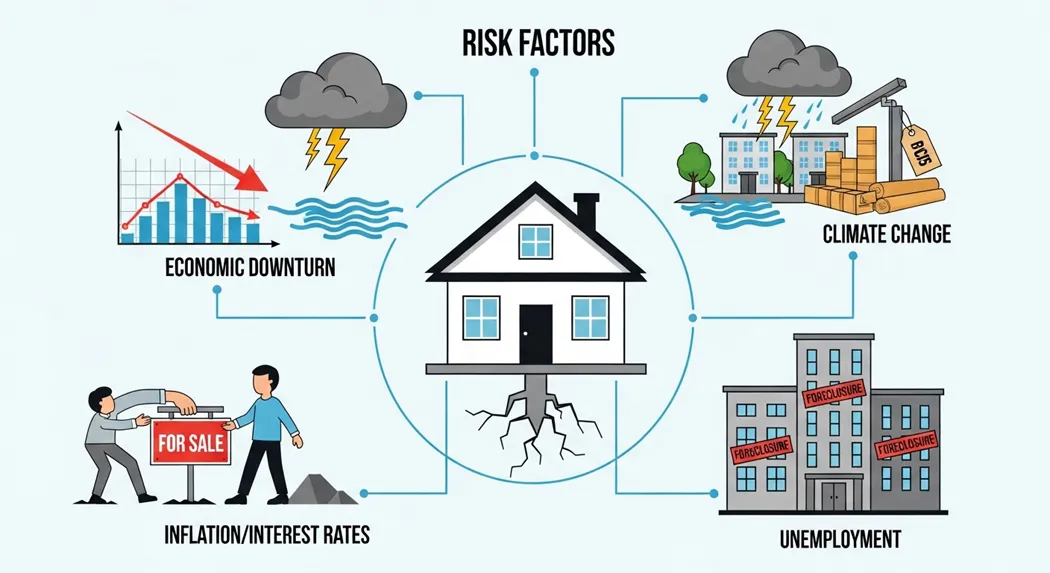

Navigating the risk factors for residential real estate markets in 2025 demands a clear-eyed approach, especially as economic shifts and policy changes reshape the landscape. Have you considered how rising unemployment could affect your property value? As a seasoned real estate analyst with over 15 years in the industry, I've seen markets boom and bust, from the 2008 housing crisis to the post-pandemic surge. Today, residential property investment risks are more pronounced than ever, driven by high home prices, interest rate volatility, and external threats like climate events.

Residential real estate market risks encompass a range of factors that can erode property values, reduce rental income, or complicate sales. These include economic downturns, location-specific vulnerabilities, and operational challenges. For instance, while home prices remain elevated in many areas, affordability strains are pushing more buyers to the sidelines, leading to slower sales and potential corrections. According to recent data, the U.S. housing market is expected to grow at a subdued pace of around 3%, with mortgage rates hovering near 6.7% by year-end. This creates a precarious environment for investors and homebuyers alike.

What are the riskiest factors for residential real estate markets? High among them are overvaluation currently at 16.5% nationally, surpassing 2006 bubble levels and foreclosure spikes, up 17% year-over-year in some reports. In Canada, similar pressures from mortgage renewals at higher rates are amplifying arrears risks. These dynamics highlight the need for due diligence. This guide explores key risks, drawing on data from sources like ATTOM and OECD analyses, to empower first-time homebuyers, investors, and professionals. While risks vary by region these factors are based on data for developed markets like the U.S. and Canada understanding them can help you make informed decisions. Remember, this is not financial advice consult a professional advisor. For more on real estate trends, see our guide on supply shocks in condo markets.

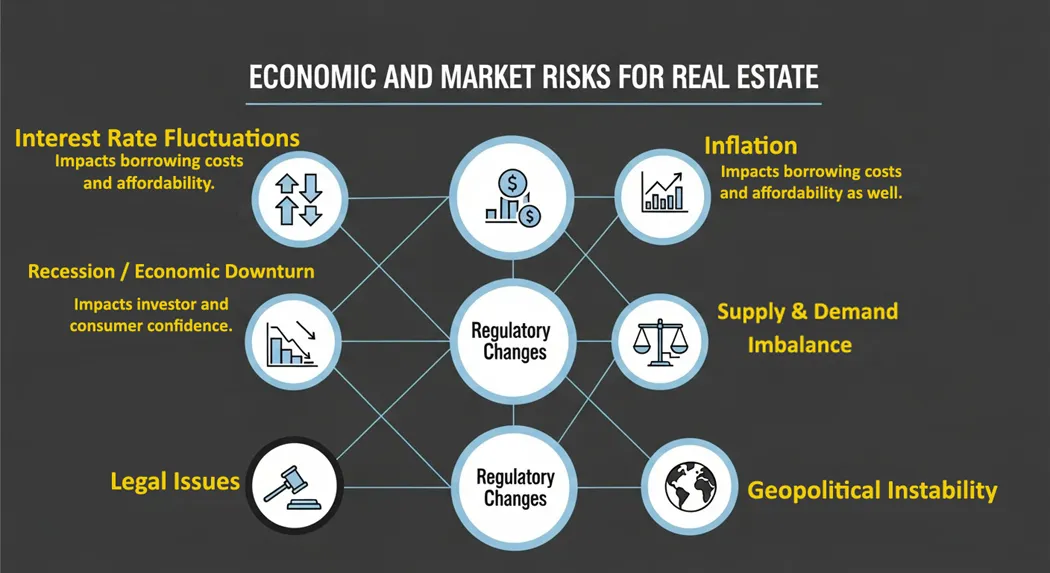

Economic factors affecting real estate are central to market stability. Recessions, inflation, and unemployment can trigger widespread declines. For example, rising unemployment rates are heightening local housing vulnerabilities, particularly in Southern U.S. states where ATTOM data shows elevated foreclosure risks.

Interest rate risks for housing markets remain acute in 2025. With rates expected to ease only modestly, borrowing costs strain affordability, locking in existing homeowners and reducing inventory turnover. Inflation exacerbates this by driving up construction and maintenance expenses, creating an inflationary feedback loop in rents and prices.

Real estate bubble risks are evident in overvalued markets. Nationally, prices are 16.5% above fundamentals, echoing pre-2008 conditions where rapid drops followed. Cities like Atlanta and Tampa face heightened crash potential due to investor retreats and policy shifts.

Location risk in real estate investing is paramount neighborhood changes can drastically impact values. Areas with declining infrastructure or shifting demographics, such as those hit by urban decay, see faster depreciation. Property condition adds another layer. Aging homes require costly updates, and in markets like California, where inventories rose 40% amid foreclosures, neglected properties amplify losses. Climate vulnerabilities, affecting over $12.7 trillion in U.S. homes, pose severe risks from floods and wildfires.

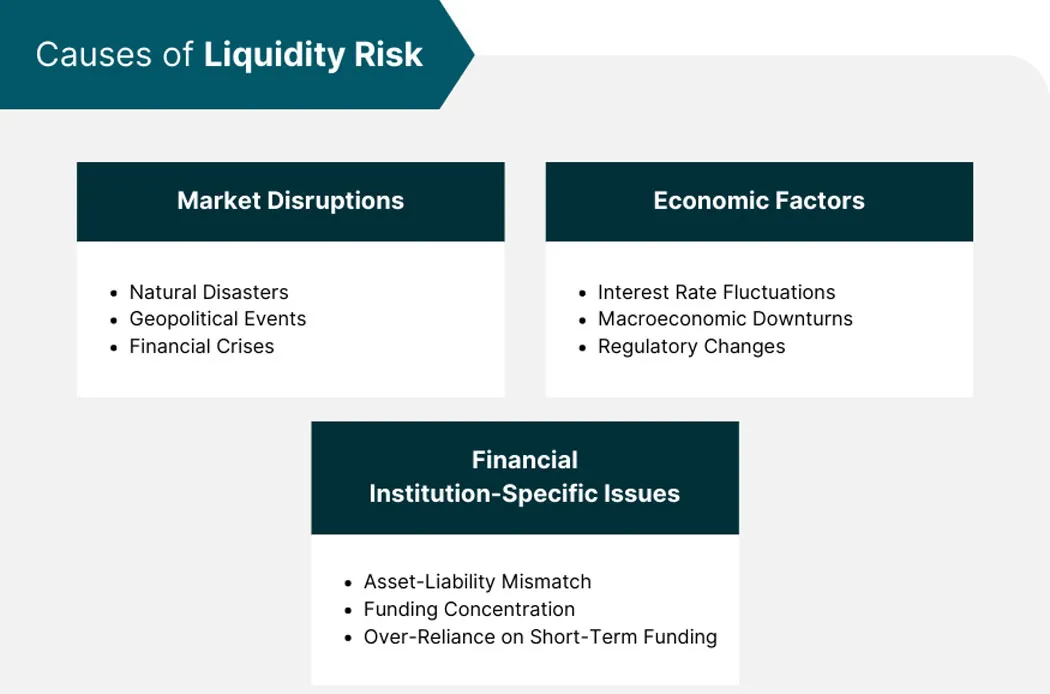

Financing risks stem from mortgage rate fluctuations and debt traps for households. In 2025, $957 billion in commercial real estate loans mature, risking defaults at higher rates. Liquidity challenges arise when selling becomes difficult; with days on market averaging 63 nationally but lower in resilient Midwest areas, sellers in overpriced regions face concessions. High consumer debt delinquencies compound this, reducing buyer pools and forcing price adjustments.

Vacancy risk in residential properties is rising, with national home vacancy rates steady at 1.3% but "zombie" foreclosures up to 3.38%. In Canada, rental reversals from mortgage stress could spike arrears. Tenant and management risks in property investment include maintenance costs and disputes. Surging insurance premiums, a top affordability strain, add operational burdens.

Legal and regulatory risks in real estate involve policy changes, like elections impacting financing costs. External threats, such as natural disasters, are amplified by climate trends, with one in four U.S. homes at severe risk. Zoning bottlenecks and foreign investment rules further constrain supply.

Types of risk in real estate often divide into structural and cyclical. Structural risks are long-term, like population declines or high housing costs relative to income, while cyclical risks fluctuate with the economy, such as debt levels or construction rates.

|

Aspect |

Cyclical Risks |

Structural Risks |

|

Definition |

Short-term economic fluctuations, e.g., interest rate hikes amplifying debt vulnerabilities. |

Persistent issues, e.g., demographic shifts reducing demand by 2030. |

|

Examples |

Recession-driven foreclosures, up 41% in 2025 |

Affordability crises from zoning limits, leading to 30 million unit shortages in some markets |

|

Impact |

Can cause rapid corrections, like 20-30% price drops in recessions |

Erode market stability over time, decoupling housing from social needs |

Market risk in real estate ties closely to cyclical elements, while structural ones demand policy interventions.

How to minimize real estate risks? Diversify investments, conduct thorough due diligence, and hedge against rates with fixed mortgages.

For comparisons, see this table on mitigation approaches:

| Risk Type | Strategy | Example Benefit |

|---|---|---|

| Economic | Diversification | Reduces recession impact by 20-30%. |

| Location | Research demographics | Avoids 10-15% value drops from shifts. |

| Financing | Rate locks | Stabilizes payments amid volatility. |

Real estate investment risks in 2025 include subdued growth, with prices rising modestly at 3% amid low demand. Beyond 2025, societal shifts like $70 trillion in boomer wealth transfers could flood markets, depressing values as millennials favor alternatives like crypto. In Canada, prolonged slowdowns and inventory surges signal corrections. While a full crash is unlikely, regional vulnerabilities persist.

In summary, the 4 key factors that drive the real estate market supply/demand, interest rates, economic health, and location interplay with risks like bubbles, vacancies, and regulations to shape 2025's landscape. Risks of investing in real estate are real but manageable with knowledge. Empower yourself by assessing personal finances and market data. For personalized strategies, consult a certified advisor. Stay vigilant, and turn risks into opportunities.

At GOAT Realty, we believe that home buying is more than just a deal. It is a journey to find the best space that fits your unique lifestyle.